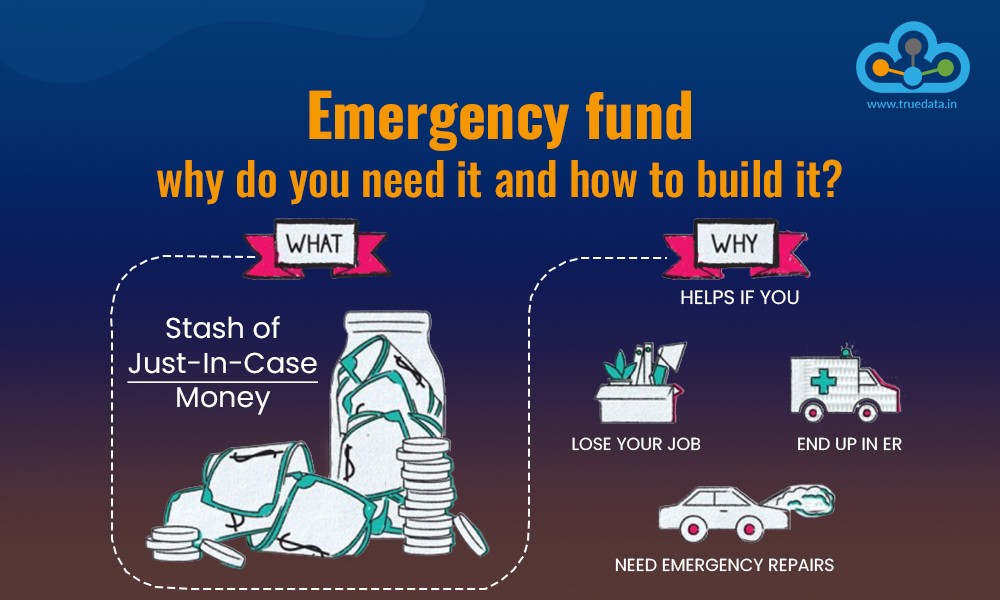

In the grand architecture of personal finance, while discussions often gravitate towards high-growth investments, retirement planning, and sophisticated wealth-building strategies, there exists a foundational pillar that, though less glamorous, is arguably the most critical: the emergency fund. This dedicated reserve of easily accessible cash is not designed for spectacular returns; its sole purpose is to act as an indispensable financial shock absorber, safeguarding individuals and families against the inevitable, yet unpredictable, crises of life. Overlooking the importance of building a robust emergency fund is akin to constructing a magnificent house without a solid foundation, leaving everything vulnerable to the first major tremor.

The most compelling argument for an emergency fund lies in its ability to provide an immediate and crucial **buffer against unexpected financial shocks**. Life is inherently unpredictable, and even the most meticulously planned budget can be derailed by unforeseen events. A sudden job loss, an unexpected major car repair, a leaky roof requiring urgent attention, or a significant medical emergency can all inflict severe financial strain. Without an emergency fund, individuals are often forced to resort to desperate measures: accumulating high-interest credit card debt, taking out predatory loans, or prematurely cashing out long-term investments, incurring penalties and derailing future financial goals. An emergency fund, conversely, allows you to navigate these crises without compounding the initial problem with additional financial burdens.

Consider a scenario where a primary breadwinner unexpectedly loses their job. The stress of unemployment is immense, but the added pressure of immediate financial obligations can be crushing. With a well-stocked emergency fund, that individual gains precious time—time to search for a new job without the immediate panic of missing mortgage payments or putting food on the table. They can make deliberate, thoughtful career decisions rather than being forced into the first available opportunity out of desperation. This bridge during periods of income disruption is one of the most invaluable services an emergency fund provides.

Beyond job loss, medical emergencies frequently underscore the fund’s importance. Even with comprehensive health insurance, deductibles, co-pays, and out-of-network charges can quickly accumulate to thousands of dollars. A sudden illness, an accident, or a necessary surgery can lead to significant out-of-pocket expenses. An emergency fund ensures that these medical crises don’t transform into financial catastrophes, allowing you to focus on recovery rather than worrying about exorbitant bills. It provides the freedom to access necessary care without succumbing to debt.

Another crucial benefit of an emergency fund is the **prevention of debt accumulation**. High-interest debt, particularly from credit cards, acts as a corrosive force, eroding financial progress. When faced with an emergency and no readily available cash, resorting to credit cards becomes the default solution. The interest charges on these balances can quickly snowball, trapping individuals in a cycle of debt that is incredibly difficult to escape, especially when they are already managing reduced income or unexpected expenses. An emergency fund serves as a crucial line of defense, allowing you to pay for unforeseen costs with cash, thereby preserving your credit score and keeping your financial future unburdened by high-interest obligations.

Furthermore, an emergency fund contributes significantly to **mental and emotional well-being**. Financial anxiety is a pervasive stressor in modern life. The constant worry about what might happen if an unexpected expense arises can take a heavy toll. Knowing that you have a financial safety net provides a profound sense of security and peace of mind. This reduced stress allows for better decision-making, improved sleep, and a greater overall capacity to enjoy life’s moments, free from the constant shadow of potential financial catastrophe. It’s an investment in your psychological resilience as much as it is in your monetary future.

The practical question then becomes: **how much should be in an emergency fund, and where should it be kept?** Financial experts generally recommend having at least three to six months’ worth of essential living expenses saved. For those with less stable incomes (e.g., freelancers, commission-based earners) or greater family responsibilities, nine to twelve months might be more prudent. “Essential living expenses” include housing costs, utilities, food, transportation, and basic insurance premiums—anything necessary to maintain your basic lifestyle. The fund should be held in an account that is **liquid and easily accessible**, such as a separate high-yield savings account. While the interest rates on these accounts are modest compared to investments, the priority is accessibility and safety, not aggressive growth. Avoid tying up emergency funds in volatile investments like stocks, as you might need the money during a market downturn, forcing you to sell at a loss.

In conclusion, while the pursuit of wealth accumulation often captures the financial spotlight, the quiet discipline of building and maintaining an emergency fund remains an indispensable, non-negotiable step on the path to true financial security. It acts as the primary defense against life’s inevitable curveballs, preventing debt, preserving investments, and, most importantly, providing the invaluable peace of mind that allows individuals and families to weather any storm without succumbing to financial despair. Neglecting this foundational element is a gamble no one should be willing to take with their financial future.